Although the term ‘affordability check’ is most commonly associated with mortgages and bank loans, they are now part of the gambling world too. In much the same way that a bank will check that a potential customer can afford monthly repayments, online bookmakers regularly check that big-staking customers can afford their level of spending (or at least they should). This is something put in place to reduce the amount of problem gambling and serve as an anti-money laundering measure as well.

Although the term ‘affordability check’ is most commonly associated with mortgages and bank loans, they are now part of the gambling world too. In much the same way that a bank will check that a potential customer can afford monthly repayments, online bookmakers regularly check that big-staking customers can afford their level of spending (or at least they should). This is something put in place to reduce the amount of problem gambling and serve as an anti-money laundering measure as well.

In addition to looking at the current status and effectiveness of affordability checks at online gambling sites, we will also look at what the future may hold for such measures. We will also explain when and how you might be subject to these.

When Do Affordability Checks Apply?

You may be contacted by your bookmaker’s customer support if additional information is required

In September 2022, the UK Gambling Commission (UKGC) updated their rules surrounding the protection of customers at risk of harm. Among these new regulations was the minimum requirement to monitor a specific range of indicators in order to identify gambling harm.

Two of these indicators are financial – customer spend and patterns of spend. In other words, gambling firms have an obligation to keep a close eye on what customers are depositing and how they spend it.

By keeping track of this information, plus the other indicators such as time spent gambling, betting sites are able to (and required to) flag customers of concern and ‘take action in a timely manner’. There is far more detailed guidance that online betting sites have to follow, outlined here but there is lack of specific thresholds mentioned.

The guidance tells operates they must “use realistic thresholds and trigger points, designed to identify those experiencing harm”. Part of this is shaped by “amounts spent compared with other customers” but ultimately there is some degree of discretion involved.

This discretionary element means that there is not an entirely consistent approach among betting sites. A customer may end up flagged at one bookmaker, online casino or other type of betting site, but not at another as internal thresholds for action are likely to differ. It is not as simple as saying a customer will face checks once they have lost £x, or deposited a certain figure in a specific timeframe, regardless of where they gamble.

It all depends on where you are betting but rarely do sites publish this kind of information, or include it within their terms and conditions. And even then we suspect there is a lot of variation in how a site applies its own guidelines. To give you some idea though, the Racing Post reported that one operator lowered their affordability check threshold to just £500, down from £2,000 in 2021.

The problem with this somewhat flexible approach is that many betting sites will only get involved at the point where they risk getting themselves in regulatory trouble. After all, betting sites primarily exist to make money, so it is not in their financial interests, certainly in the short term, to clamp down on a player who is losing substantial sums.

What Happens if Bookmakers Don’t Carry Out Checks?

Gambling Commission fines for failing to complete checks can run into millions of pounds

Not adhering to rules on affordability checks comes with big fines, although there have been numerous instances of firms failing to take anything close to satisfactory action. Whether an intentional blind eye or the fault of poor processes/staff shortages, it is alarming just how often affordability checks are not carried out when they should be.

Just to give you some more recent examples, one operator faced a £3.25m fine in July 2023, partly for not carrying out any checks on a player who bet over £500,000 during a two-month period. Similarly, another took a record £19.2m hit for various failings, many of which involved letting players spend tens of thousands without any checks whatsoever. One customer lost £54,252 in four weeks without any steps to identify the risk of harm.

The examples are plentiful as this is an area where online betting sites have repeatedly fallen foul of the rules. It should be stressed though this only represents a minority of gambling businesses, as most do carry out the checks at appropriate times. Handing out such large fines as a deterrent does work quite well it would seem!

Why Have Affordability Checks Been Introduced?

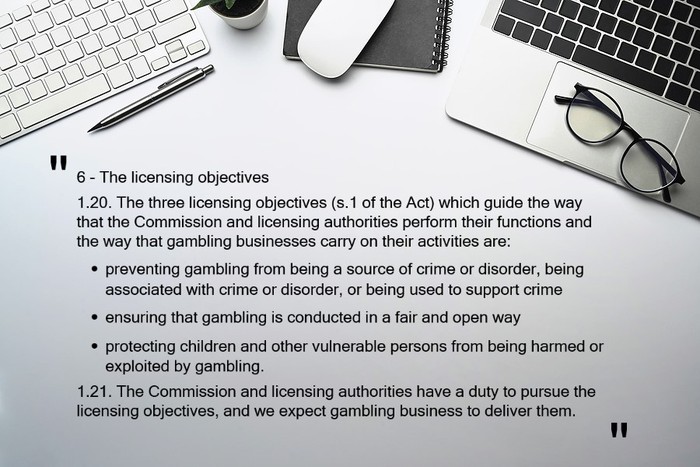

The Gambling Commission has three key licensing objectives

Based on the large fines the Gambling Commission dishes out for non-compliance, it is easy to see that affordability checks are high on their list of priorities. The reason for this is two-fold. Checks not only protect customers but they are also an important part of any anti-money laundering policy.

A betting firm that is lax on its affordability checks is not only putting players at risk but it is potentially allowing illegal money to flow through its systems. The UKGC has a stated role that includes trying to separate criminality from gambling and so this is an important issue within the industry.

Preventing Financial Harm

Even the Gambling Commission understands that in order to survive, betting sites have to make money. For them to do this, customers as a whole must lose more than they win. Players registering a net loss is not inherently problematic, it is only an issue if they are losing money they cannot afford.

If customers, often those addicted to gambling, are spending well above their means, this is where immediate action needs taking. Not only does gambling lose its fun aspect but such players can end up facing real financial hardship should their bets end up as losers.

Preventing financial hardship caused by betting is one of the key objectives of the Gambling Commission and it is why they require sites to carry out checks where appropriate.

Preventing Money Laundering

The other issue with allowing a player to spend large sums of money without checks is that it attracts illegally sourced money. Betting websites offer a way to ‘clean’ money, giving itself distance from its illegal source. Alternatively, they can simply be used by genuine customers but ones that are funding their accounts through illegal means. Such behaviour is easily discouraged though by affordability/source of wealth checks. If a player cannot prove how they are funding such expensive bets, a bookmaker will (or at least should) close their account down and/or prompt further investigation.

How Do Bookmakers Carry Out Affordability Checks?

Documents can be submitted electronically and securely

We have looked at why affordability checks exist and the guidance surrounding them but what do they entail exactly? Currently, the most common approach is just to request financial documentation from customers. This can include things such as recent payslips, P60s, bank statements, employment contracts, tax returns and the like.

Although players only have to send digital copies via secure portals, rather than originals in the post, many do not like their intrusive nature as reported by the Racing Post. Many legitimate punters feel that it is their money and they should be free to do what they want with it without these, as they see them, invasions of privacy. This is an understandable sentiment but ignores the fact that whilst they may not have any issues themselves, nor be betting illegally, other people are – and some form of action needs to be taken.

What About In-Store Bookmakers?

The rules discussed above relate to online operations, however checks will still be applied to high street bookmakers also. Such affordability checks do occur at physical betting outlets whether it be those on the high street or those beside a racetrack though it is not feasible for this to be done at such specific limits as it can be with an online operator.

Future Plans

The UK government’s Gambling Act Review white paper was published in April 2023

At the time of writing, the UK Government’s Gambling Act Review White Paper was still in its consultation phase. With updates to the Gambling Act 2005 set to be significant and covering many different areas, unsurprisingly one focus has been on affordability checks. Following discussions with the Gambling Commission, the suggestions relating to affordability include the introduction of two new checks.

Financial Vulnerability Check

First would be a light touch financial vulnerability check. Through this, bookmakers would carry out unintrusive checks using publicly available data. The proposal is that bookmakers would have to carry out such checks when a player hits a £125 net loss during a rolling 30-day period or £500 within a 365-day period. Some larger bookmakers carry out these ‘light touch’ financial checks for all players at registration anyway, so it would impose no additional administrative costs for them. Others, however, only do it later on in the customer journey.

Financial Risk Assessment

The other step that has been proposed is a financial risk assessment. The suggested threshold for this more substantial check is when a player’s losses exceed £1,000 in a rolling 24-hour period or £2,000 within a 90-day period. Although this will apply to most players, the plan is to have lower trigger amounts for any customer aged between 18 and 24. The check itself would involve acquiring credit reference agency data. This would give bookmakers insight into a player’s financial situation, thus enabling them to understand more the potential risk of harm involved. This, of course, would be more invasive from a customer perspective, and also more costly to betting companies.

Should Bookmakers Carry Out Financial Checks?

Although the above plans remain in a consultation stage there does seem to be a real appetite to push forward with some form of affordability check. Therefore, do not be surprised if these, or similar measures are soon made into law. For punters concerned about this, and there are plenty, the UKGC has sought to play down their concerns.

They pointed out that only around 20% of accounts would be subject to the light touch check and only around 3% would face a financial risk assessment. In the case of the latter, at least 80% of these will happen behind the scenes with credit reference agencies, making them entirely frictionless. An additional 10% will be carried out through third-party open-source banking, which again requires virtually no customer involvement, only giving their consent.

Overall, the Gambling Commission estimates that only 0.3% of players would have to supply financial information to a bookmaker, whether this be recent payslips or bank statements. As with the current rules though, this will only apply to online bookies and not those on the high street or at racecourses.

If you want to know how about the affordability proposals, the Gambling Commission has a detailed FAQ page on their website.